Subscribe and receive email notifications of new blog posts.

RSS Feed

RSS Feed

9

May 2026 Alabama Gulf Coast Real Estate Stats

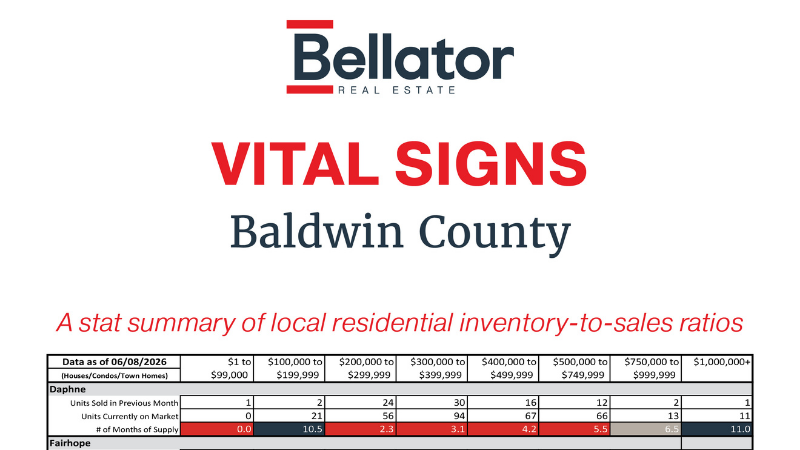

Vital Signs provides a visual representation of what's happening in the Alabama Gulf Coast real estate market. The color-coded numbers represent the absorption rate; the number of months it would take to sell every home on the market in a particular price range if no others were added. If the market is moving quickly, the absorption rate will fall below six months of supply, and if it's more of a buyer's market, it will jump above six months of supply. The rate is determined by dividing the number of units currently on the market by the number sold in the past month.

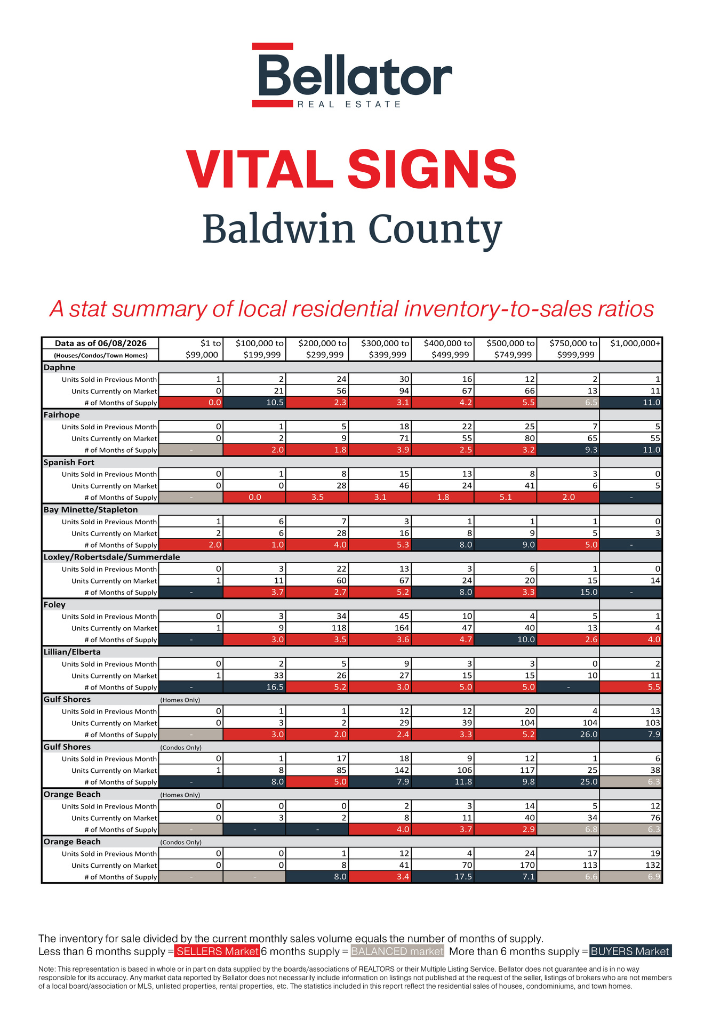

Baldwin County Real Estate Market Update

Comparing April vs. May 2026 Housing Trends

As Baldwin County moves deeper into the summer selling season, the May 2026 market data reveals a familiar trend: increased buyer activity across many communities, particularly in the mid-price ranges where demand remains strongest. While inventory continued to grow in several markets, sales activity generally kept pace, helping maintain balanced conditions across much of the county.

The story of May was one of strong absorption in the $200,000 to $500,000 price ranges, continued luxury market activity along the coast, and growing opportunities for buyers as inventory expands in select areas.

Let's take a closer look at how Baldwin County performed from April to May.

Market Overview

Countywide, May brought:

- Strong sales growth in many primary residential markets

- Increased inventory in several communities

- Continued demand in the $200,000 to $500,000 price ranges

- Improved absorption rates in many luxury and coastal segments

- More balanced conditions overall compared to earlier in the year

The strongest activity continued to occur in the $200,000 to $399,999 range, particularly in Daphne, Foley, Spanish Fort, and Loxley/Robertsdale/Summerdale.

Daphne

Daphne experienced one of its strongest months of the year.

Key Highlights:

- Sales in the $200K–$299K range increased from 13 to 24 units.

- $300K–$399K sales jumped from 16 to 30 units.

- Inventory increased, particularly in the $300K–$499K ranges.

Despite higher inventory levels, months of supply improved significantly:

- $200K–$299K dropped from 4.7 months to 2.3 months.

- $300K–$399K improved from 4.9 months to 3.1 months.

Takeaway:

Buyer demand surged in Daphne during May, making it one of the county's most active markets.

Fairhope

Fairhope continued to show strong activity, especially among move-up and luxury buyers.

Notable Changes:

- $400K–$499K sales increased dramatically from 7 to 22 units.

- $500K–$749K sales rose from 17 to 25 units.

- Inventory remained relatively stable.

Months of supply improved considerably:

- $400K–$499K fell from 7.7 months to 2.5 months.

- $500K–$749K decreased from 5.2 months to 3.2 months.

Takeaway:

Fairhope's upper-middle price ranges remain exceptionally attractive to buyers, with strong absorption keeping pace with inventory.

Spanish Fort

Spanish Fort posted another strong month with broad-based gains.

Highlights:

- $300K–$399K sales nearly doubled from 8 to 15.

- $400K–$499K sales more than doubled from 6 to 13.

- Inventory remained relatively stable.

Months of supply improved:

- $300K–$399K fell from 5.5 to 3.1 months.

- $400K–$499K dropped from 4.2 to 1.8 months.

Takeaway:

Spanish Fort remains one of Baldwin County's strongest seller-friendly markets.

Bay Minette & Stapleton

Activity remained healthy but mixed.

Key Trends:

- Sales under $200K remained strong.

- Inventory remained stable across most categories.

- Some price ranges experienced slower absorption.

The $200K–$299K segment saw months of supply rise from 3.4 to 4.0 months, while inventory remained relatively unchanged.

Takeaway:

Bay Minette and Stapleton continue to offer affordability and value, although conditions vary by price point.

Loxley, Robertsdale & Summerdale

This growing corridor continued to attract significant buyer interest.

Notable Changes:

- $200K–$299K sales remained robust with 22 transactions.

- Sales above $500K increased noticeably.

- Inventory declined in the $200K–$299K category.

Months of supply improved:

- $200K–$299K dropped from 2.3 to 2.7 months despite higher sales volume.

- Higher-end inventory remains elevated.

Takeaway:

The central Baldwin growth corridor continues benefiting from affordability and new construction opportunities.

Foley

Foley remained one of Baldwin County's highest-volume markets.

Highlights:

- 34 homes sold in the $200K–$299K range.

- 45 homes sold in the $300K–$399K range.

- Inventory declined in several key categories.

Months of supply improved:

- $300K–$399K fell from 4.2 to 3.6 months.

- $400K–$499K improved from 6.0 to 4.7 months.

Takeaway:

Foley continues to attract strong buyer demand and remains one of the county's most balanced markets.

Lillian & Elberta

This market showed mixed results in May.

Key Observations:

- Inventory decreased in several price ranges.

- Sales improved in the $300K–$399K category.

- Lower-priced inventory remains plentiful relative to demand.

Months of supply improved:

- $300K–$399K fell from 5.1 months to 3.0 months.

Takeaway:

Lillian and Elberta continue offering opportunities for buyers seeking affordability and lower competition.

Gulf Shores Homes

The Gulf Shores single-family home market remained active.

Major Trends:

- Luxury sales above $1 million more than doubled from 6 to 13.

- $500K–$749K sales jumped from 12 to 20.

- Inventory remained relatively stable.

Months of supply improved significantly:

- $500K–$749K dropped from 9.4 to 5.2 months.

Takeaway:

Luxury and upper-end buyers were highly active in Gulf Shores during May.

Gulf Shores Condos

The condo market showed continued improvement.

Highlights:

- Sales increased across nearly every price category.

- $200K–$299K sales rose from 14 to 17.

- $300K–$399K sales climbed from 16 to 18.

Months of supply improved:

- $300K–$399K fell from 9.1 to 7.9 months.

- $1M+ inventory became much more balanced, dropping from 11.3 to 6.3 months.

Takeaway:

Buyer confidence appears to be strengthening in the Gulf Shores condo market.

Orange Beach Homes

Orange Beach's luxury market remained exceptionally strong.

Key Highlights:

- $500K–$749K sales increased from 6 to 14.

- Luxury sales above $1 million remained robust with 12 closings.

- Inventory remained relatively stable.

Months of supply improved:

- $500K–$749K dropped from 7.3 to 2.9 months.

Takeaway:

Orange Beach continues to see strong demand from luxury and second-home buyers.

Orange Beach Condos

Perhaps the biggest story of the month was Orange Beach's condo market.

Notable Improvements:

- $500K–$749K sales increased from 23 to 24.

- $750K–$999K sales more than doubled from 8 to 17.

- $1M+ sales remained extremely strong with 19 closings.

Months of supply improved dramatically:

- $300K–$399K fell from 5.2 to 3.4 months.

- $750K–$999K dropped from 16.6 to 6.6 months.

- $1M+ inventory increased from 6.0 to 6.9 months despite continued sales activity.

Takeaway:

The Orange Beach condo market remains one of the strongest luxury segments along the Alabama Gulf Coast.

What This Means for Buyers and Sellers

For Buyers

- Inventory is growing in many markets, creating more options.

- Some coastal luxury segments offer increased selection compared to earlier in the year.

- Well-priced homes still move quickly in the $200K–$500K range.

For Sellers

- Demand remains strong throughout Baldwin County.

- Proper pricing continues to be critical as inventory expands.

- Coastal and luxury properties are seeing healthy buyer activity, especially in Gulf Shores and Orange Beach.

Final Thoughts

May 2026 showcased a Baldwin County market that continues to benefit from strong buyer demand, steady inventory growth, and healthy sales activity across nearly every major community. The strongest performance came from Daphne, Fairhope, Spanish Fort, Foley, and the coastal luxury markets, where buyers remained active despite rising inventory levels.

As summer begins, Baldwin County remains one of Alabama's most dynamic real estate markets, offering opportunities for both buyers and sellers across a wide range of price points and property types. The market is becoming more balanced, but in many segments, particularly between $200,000 and $500,000, competition remains alive and well.

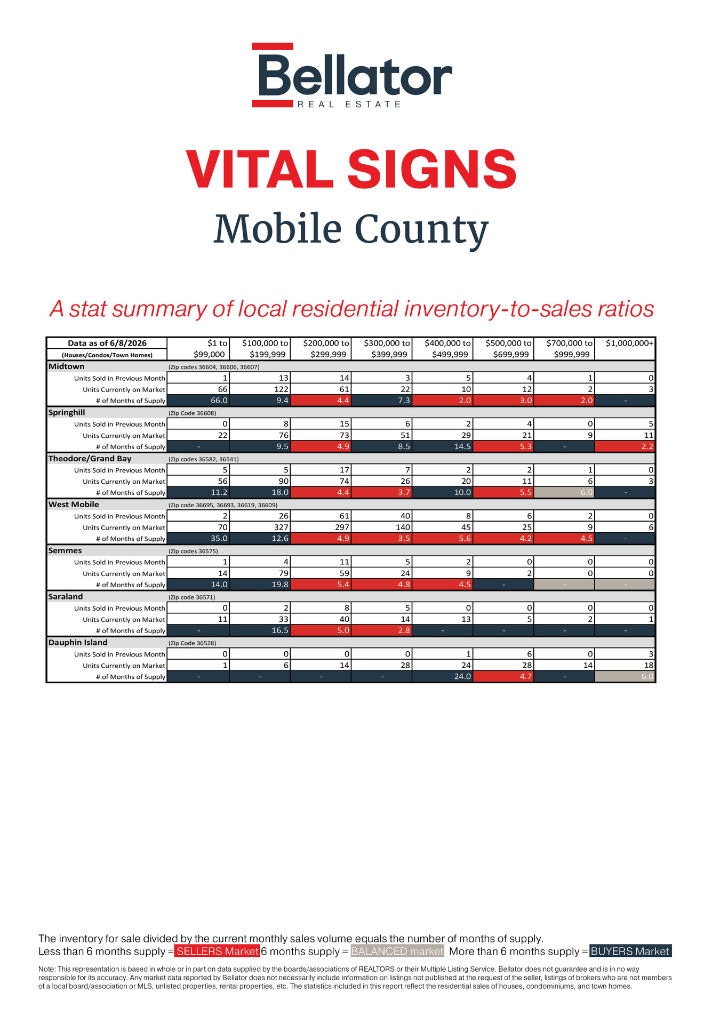

Mobile County Market Update: Comparing April vs. May 2026 Real Estate Trends

As we move deeper into the summer selling season, Mobile County's housing market continued to gain momentum in several key areas during May. Sales activity increased across many price ranges, particularly in West Mobile, Midtown, Springhill, and Theodore/Grand Bay, while inventory remained relatively stable. Overall, the data suggests that buyer demand strengthened in many segments, leading to lower months of supply and a more balanced market in several communities.

Here's a closer look at how Mobile County performed from April to May 2026.

Market Overview

The biggest story in May was increased buyer activity across many of Mobile County's most active markets.

Several areas saw substantial jumps in sales, particularly in the $100,000 to $399,999 price ranges, which remain the most active segments of the market. Inventory levels changed only modestly in most areas, meaning stronger demand translated directly into lower months of supply and improving market conditions for sellers.

West Mobile once again led the county in transaction volume, while Midtown and Springhill experienced significant improvements in market balance. Waterfront and luxury markets remained active but continued to show greater variability due to smaller numbers of transactions.

Midtown

Midtown saw a notable increase in buyer activity during May.

Sales in the $200,000-$299,999 segment rose from 8 to 14 units, while the $400,000-$499,999 category increased from 1 sale to 5 sales. Inventory declined in several price ranges, helping months of supply improve dramatically.

Notable changes included:

- $200,000-$299,999 supply dropped from 8.9 months to 4.4 months

- $400,000-$499,999 supply fell from 12.0 months to 2.0 months

- $500,000-$699,999 supply declined from 12.0 months to 3.0 months

Takeaway: Midtown moved noticeably closer toward balanced market conditions, especially in the mid-range and upper-mid-range price points.

Springhill

Springhill remained one of Mobile County's strongest performing markets.

Sales increased in the luxury segment, with the $1 million+ category jumping from zero sales in April to five sales in May. Mid-range activity also remained healthy, with 15 homes sold in the $200,000-$299,999 range.

Inventory remained stable overall, while months of supply improved in several categories:

- $200,000-$299,999 supply decreased from 5.8 months to 4.9 months

- Luxury inventory shifted from no measurable absorption to 2.2 months of supply

- Higher-end inventory remained healthy despite continued sales activity

Takeaway: Springhill continues to attract buyers across a wide range of price points, including luxury properties.

Theodore / Grand Bay

Theodore and Grand Bay continued to show steady growth.

Sales increased substantially in the entry-level market, with:

- $1-$99,000 sales increasing from 2 to 5

- $300,000-$399,999 sales increasing from 4 to 7

- Overall demand remaining strong throughout most price ranges

Months of supply improved in several key categories:

- $200,000-$299,999 supply fell from 6.5 months to 4.4 months

- $300,000-$399,999 supply dropped from 7.0 months to 3.7 months

- $500,000-$699,999 supply improved slightly from 6.0 to 5.5 months

Takeaway: Theodore and Grand Bay remain among the more balanced markets in Mobile County, particularly for homes under $400,000.

West Mobile

West Mobile once again dominated Mobile County in total sales volume.

Buyer activity surged across multiple price points:

- $100,000-$199,999 sales increased from 22 to 26

- $200,000-$299,999 sales jumped from 45 to 61

- $300,000-$399,999 sales climbed from 32 to 40

Inventory remained remarkably stable despite higher sales volume.

Months of supply improved throughout much of the market:

- $100,000-$199,999 supply decreased from 14.9 months to 12.6 months

- $200,000-$299,999 supply fell from 6.6 months to 4.9 months

- $300,000-$399,999 supply dropped from 4.6 months to 3.5 months

- $500,000-$699,999 supply improved from 4.7 months to 4.2 months

Takeaway: West Mobile continues to be Mobile County's strongest and most active residential market, particularly in the $200,000-$400,000 range.

Semmes

Semmes experienced mixed results during May.

Sales activity remained relatively stable, although transactions in the $100,000-$199,999 range increased from one sale to four sales.

Inventory changed very little, and months of supply remained elevated in some segments:

- $200,000-$299,999 supply remained near balanced at 5.4 months

- $300,000-$399,999 supply improved from 6.5 months to 4.8 months

- $400,000-$499,999 supply increased from 3.0 months to 4.5 months

Takeaway: Semmes remains relatively balanced in its core price ranges, though lower-priced inventory continues to outpace demand.

Saraland

Saraland maintained steady activity during May.

Sales improved in the $300,000-$399,999 segment, increasing from three sales to five sales, while inventory remained largely unchanged.

Months of supply improved in key areas:

- $300,000-$399,999 supply declined from 4.3 months to 2.8 months

- $200,000-$299,999 supply improved from 4.2 months to 5.0 months, remaining near balanced conditions

Takeaway: Saraland continues to offer relatively balanced conditions for both buyers and sellers, particularly in the mid-priced market.

Dauphin Island

Dauphin Island remained one of the county's most unique and volatile markets due to its smaller inventory base.

May saw increased luxury activity:

- $500,000-$699,999 sales rose from 2 to 6

- $1 million+ sales increased from 1 to 3

Months of supply improved significantly in several categories:

- $500,000-$699,999 supply dropped from 15.5 months to 4.7 months

- $1 million+ supply fell from 18.0 months to 6.0 months

However, several lower-priced categories recorded little or no sales activity, resulting in elevated inventory levels.

Takeaway: Waterfront and luxury demand strengthened considerably during May, helping absorb inventory that had accumulated earlier in the year.

What This Means for Buyers and Sellers

For Sellers

May's data shows continued momentum throughout much of Mobile County. Sellers in Midtown, Springhill, West Mobile, Theodore/Grand Bay, and Saraland are benefiting from stronger buyer demand and improving absorption rates. Proper pricing remains critical, but many segments are moving closer to seller-favorable conditions.

For Buyers

Inventory remains available throughout Mobile County, especially in higher price ranges and luxury segments. Buyers still have opportunities to negotiate in some areas, but increased sales activity suggests that desirable properties are moving more quickly than earlier this year.

Looking Ahead

The Mobile County market continues to follow a typical spring pattern, with stronger buyer demand emerging across much of the county. West Mobile remains the volume leader, while Midtown and Springhill have seen some of the most significant improvements in market balance. Theodore/Grand Bay and Saraland continue to offer stable conditions, and luxury activity is gaining momentum on Dauphin Island.

As we continue into the summer selling season, inventory levels and buyer activity will be key indicators to watch. If current trends continue, many Mobile County markets could see even tighter conditions in the most desirable price ranges over the coming months.

Contact your Bellator agent today to strategize your next move to the Gulf Coast.

Privacy Policy / DMCA Notice / ADA Accessibility